What I Learned From These Best Fintech Onboarding Processes

After working with fintech customers, we know how they struggle with onboarding.

The process must comply with strict Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. But if it’s too stretched out, it will take too long for users to use the app, making them drop off early.

As a result, the “sweet spot” is a bittersweet onboarding process that’s shorter, but still requires users to provide personal details, do identity checks, and connect bank accounts.

So, to provide a clear idea of what a good onboarding looks like in fintech, I’ll cover the common challenges in the industry, explain the onboarding process of the most popular fintech companies, and explain the user onboarding best practices in the current market.

What is the onboarding process for fintech?

The onboarding process is a series of steps to introduce a new user to a product’s core features and set up their account. It often involves in-app walkthroughs, tooltips, or other UI elements to guide users through the product.

However, unlike other industries, onboarding processes in Fintech must collect a certain level of personal data in order to stay compliant and prevent fraud (e.g., KYC verification). This inevitably introduces some friction to users, making it necessary to minimize friction as much as possible during their first session.

What’s the current onboarding state for fintech products?

Since users manage their money in fintech apps, worries about data privacy, cybersecurity, and compliance are higher than in other industries. This means onboarding users in Fintech successfully is more about making them feel safe when using your app.

But if we look at the data, there are strong reasons to believe that companies are having a harder time onboarding new users:

- Fenergo’s 2025 Financial Crime Industry Report shows 70% of finance companies lost clients due to inefficient onboarding (up from 67% in 2024 and 48% in 2023), even with an increase in AI adoption.

- 92% of people are worried about sharing too much personal data with the bank, which leads to to 21% of them abandoning the app because of it.

- APAC fraud is increasing 73%, with synthetic identity fraud jumping by 142% in a single year. The fraud rate has reached 2.5% according to Sumsub.

- The average time before a consumer gives up on a financial application is now 18 minutes 53 seconds, seven minutes faster than in 2020.

- The average mobile fintech onboarding involves 14 screens, 29 clicks, and 16 required form fields, crossing roughly 6 minutes (Incognia Friction Index).

This means implementing an effective Fintech onboarding process comes down to overcoming three significant challenges: KYC verification, regulatory fragmentation, and fraud prevention.

The 3 most impactful challenges in fintech onboarding

Now, this guide breaks down how these three challenges affect the onboarding processes in Fintech apps:

KYC and document verification create the biggest friction

KYC verification is the single largest source of friction in fintech onboarding. The process demands users to perform several technically challenging tasks in sequence. These include photographing government IDs, taking selfies, passing liveness checks, and providing proof of address.

This makes it very easy for users to abandon the app due to:

- Document capture failures: Because users struggle with blur, glare, shadows, poor lighting, and framing errors (not capturing all four document corners). And since most apps don’t give real-time feedback on pictures, one single failed document upload can trigger complete abandonment.

- Selfie and liveness verification: This introduces additional failure modes: poor lighting creating silhouettes, lack of utility bills/bank statements readily available, glasses causing reflections, and appearance changing from the ID photo. For this reason, only 29% of users report a good experience with NFC-based ID verification, and just 50% rate video verification positively (as per Signicat report).

- Privacy concerns: As mentioned, 92% of users are worried about the amount of personal data they share with Fintech products, leading to 21% dropping off. In fact, as per Signicat’s report, over half of consumers accept that reducing fraud justifies a complex application, but without transparency about purpose, they bail.

Compliance demands stack friction that product teams cannot simply remove

Unlike B2B SaaS products, fintech product teams cannot freely eliminate steps.

Besides KYC verification, fintech teams also need to comply with AML, FATCA, PSD2, GDPR, and jurisdiction-specific licensing requirements. This creates a compliance floor that prevents the onboarding experience from becoming user-friendly.

This problem is multi-factorial, introducing multiple problems at once, including:

- Compliance costs: Global AML compliance costs reached $206.1 billion in 2023, with the average fintech firm spending $11.45 million annually on AML alone, just to avoid fines that would be much more expensive.

- Regulatory fragmentation across regions: U.S. fintechs must navigate state-by-state money transmission licensing on top of federal BSA and PATRIOT Act requirements. The EU imposes GDPR data minimization rules that directly conflict with AML data collection mandates (with no clear resolution). This means any fintech operating across multiple markets must maintain parallel compliance flows, each adding potential friction.

- Tax reporting requirements: IRS forms W-8 and W-9 are written in technical legalese that non-native English speakers and typical consumers struggle to parse. Plus, FATCA/CRS self-certification forms collected during user onboarding are often not reviewed until days after account opening, requiring multiple follow-up contacts that add more friction.

Fraud is surging and it directly shapes onboarding design

As mentioned, identity theft/fraud in Fintech onboarding is escalating rapidly, with 67% of financial institutions reporting fraud in 2025. The sophistication of attacks is what makes the onboarding design challenge so acute.

These fraud attempts are becoming more sophisticated over time, increasing the magnitude of this challenge to the point that it might become inevitable. Some common fraud strategies include:

- Synthetic identity fraud: Where criminals combine real and fabricated information to create entirely new identities. What’s worse, approximately 95% of synthetic identities pass through standard onboarding checks, and an estimated 2.5 million synthetic identities currently sit in U.S. bank accounts, according to the FDIC.

- Deepfake fraud: Businesses report a 200% surge in deepfake-aided wire fraud attempts in Q1 2025. There’s a “Fraud-as-a-Service” underground market that now sells subscription-based tools for account takeovers, synthetic identity creation, and deepfake generation, democratizing sophisticated fraud techniques.

How do the best fintech companies address the onboarding process?

Now we’re going to look at how different companies navigate the onboarding process. And to explore different cases, I’ll cover companies in both B2B and B2C markets for banking and payments.

That said, keep in mind that many of these companies are far from perfect, but there are still one or two practices to learn from.

Let’s start with Gusto:

Gusto

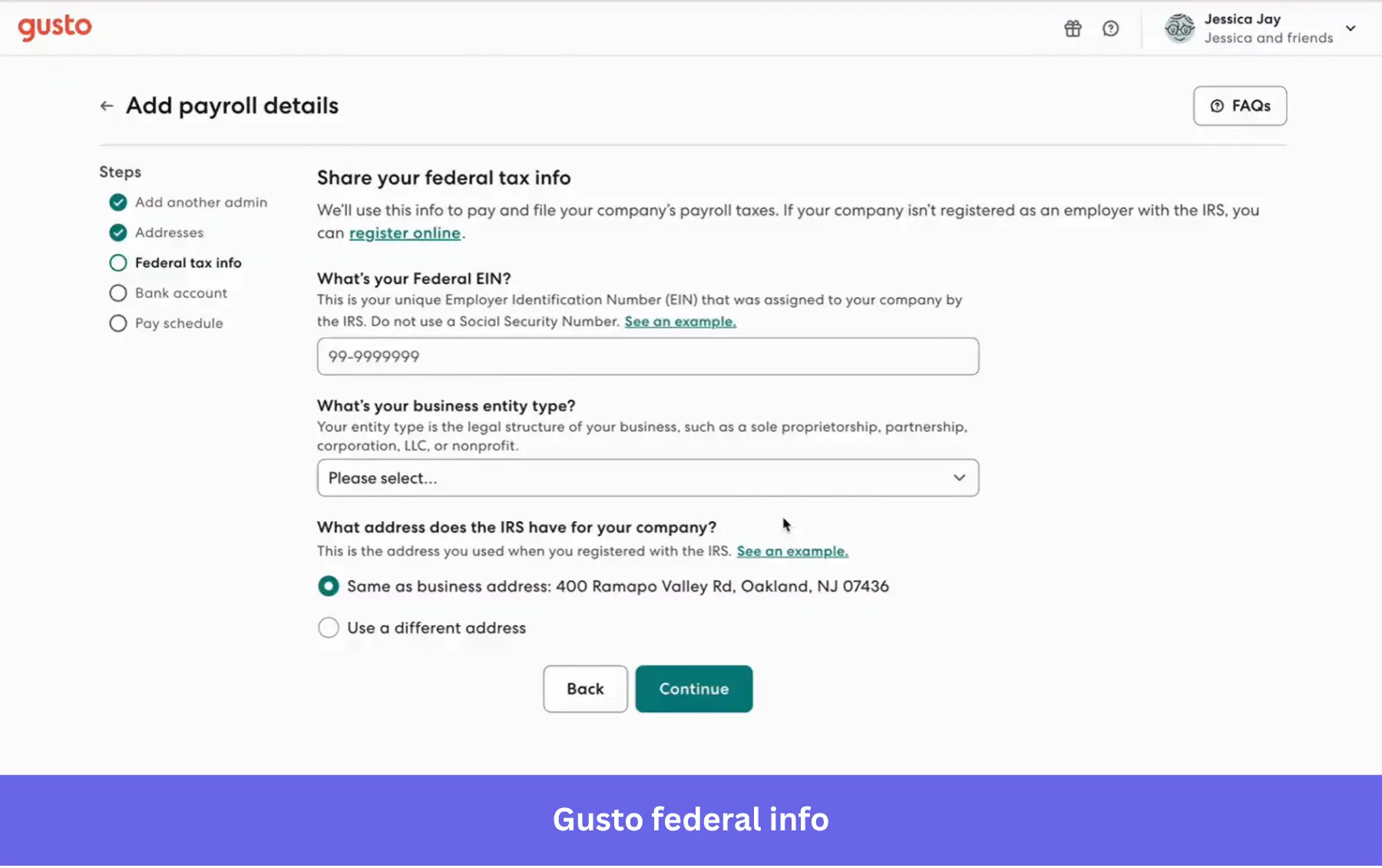

Gusto is an HR and financial service for US businesses that need to streamline payroll, employee benefits, and accounting.

As an HR-focused business with even more compliance requirements, I naturally found the onboarding process to be very lengthy. It asks for a lot of business information, such as:

- Who are you going to pay.

- US states where you operate.

- Whether you’re registered as an employer with the IRS.

- Your official industry.

- Whether your product is related to cannabis.

That said, I appreciated the fact that, instead of handing an endless form to fill out, it broke the entire onboarding flow into quick questions I could answer quickly. Plus, the platform offered me a personalized package based on my data and immediately walked me through the account setup (i.e., adding company address, other admins, tax info, etc.) to start using the product.

Still, I believe Gusto could afford to break down the process a lot more. The tax info, for example, could’ve been collected later after landing inside the product. There was no need to collect so much info upfront.

Starling bank

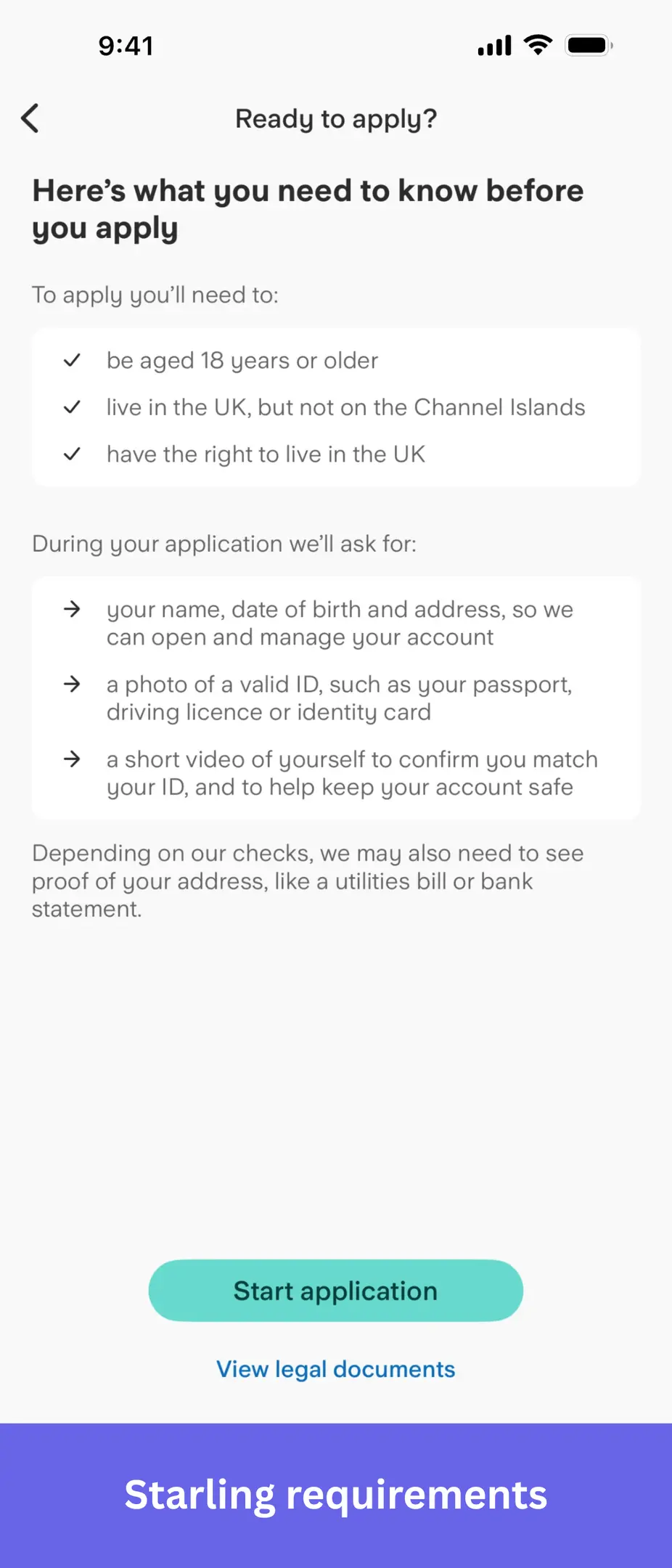

Starling is a UK-based mobile budgeting app that allows you to save money inside dedicated “Spaces”, create a bank account, and get a card.

The onboarding flow for personal accounts was also very long. It starts with an application flow that starts by introducing the product features, then asks for the documentation needed to apply, KYC verification, and extra info about my income.

I liked the fact that it focused on explaining the value of the product upfront (i.e., how you can save money easily), and how it showed me the list of required documents before proceeding with the application. This way, I could verify if I had everything I needed and come back later if it wasn’t the right moment, preventing me from the frustration of hitting an unexpected wall.

That said, the process is still unnecessarily lengthy. It could ask about my income later, after creating my first space, for example. Also, many fintech apps allow users to complete their KYC verification after landing inside the app (just before they can link their bank account or make a transaction), I can’t see why this app should be an exception.

Paypal

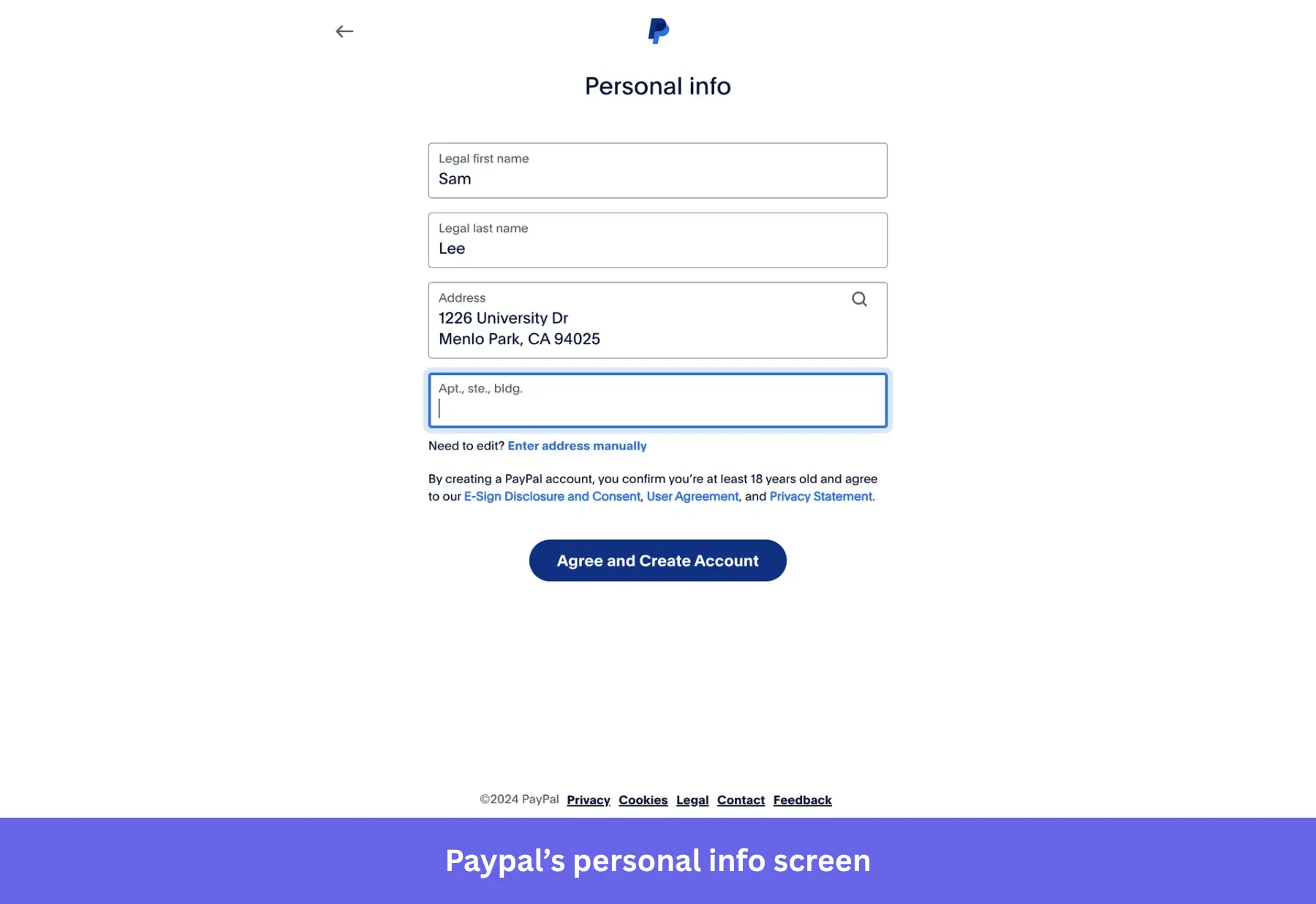

Since Paypal’s platform is simpler (no setting up bank accounts), they can afford to ask for less upfront information during account creation.

For a mainstream platform like Paypal, I really appreciate the simplicity. The onboarding process started asking me if my account is personal or business, then proceeded to ask for basic information, including:

- Email.

- Phone number (with verification).

- Password creation.

- Legal name and address (no utility bill needed).

- Card info/account numbers to link to your account.

Once done, I only needed to create a unique username to start sending and receiving payments globally. I’m free to link a bank account or a card whenever I need. In fact, unverified accounts can send up to $4,000 USDs per transaction, so you really can take your time with it.

The only missing part in my book is some form of personalization. But Paypal is a big enough company to avoid this entirely without falling short.

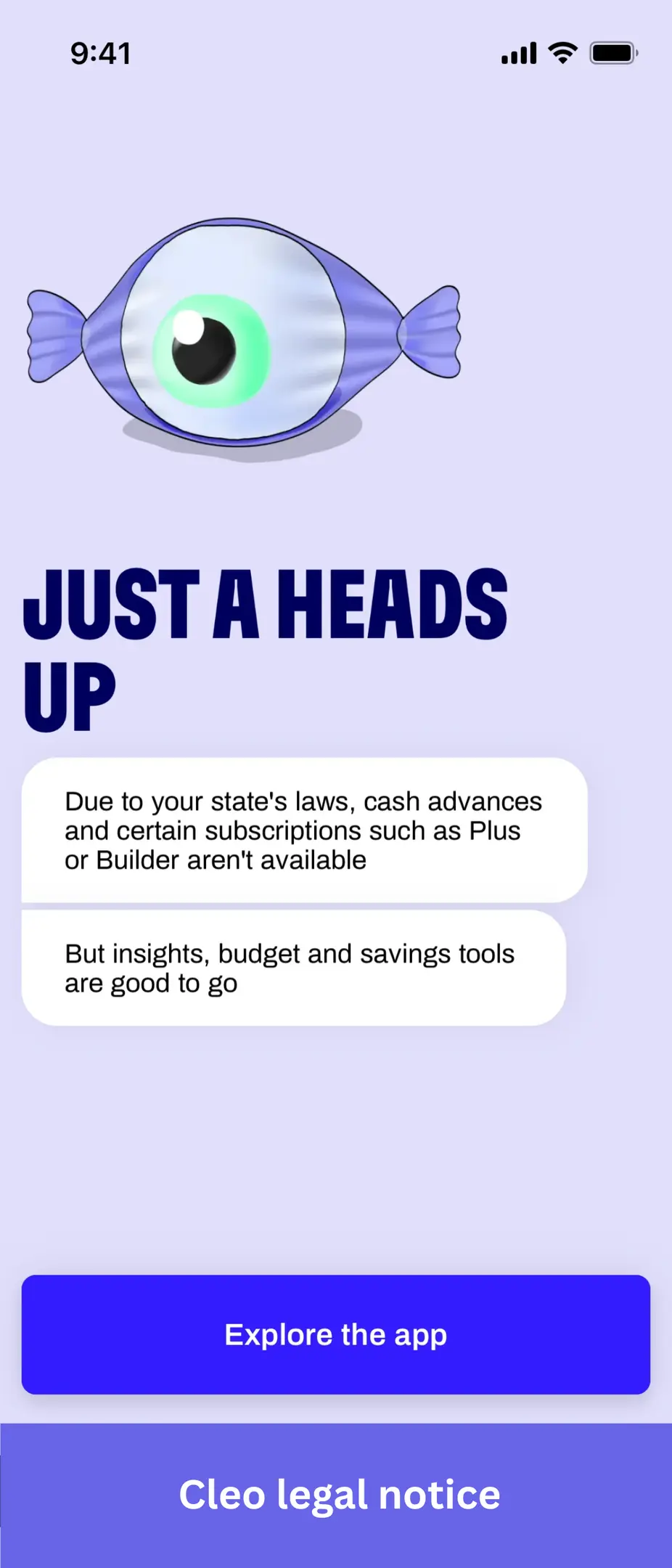

Cleo

Cleo is a mobile assistant that analyzes your transactions and gives you advice to save money, with a card that lets you set spending limits.

Thankfully, as an expense tracker without payment processing or a bank account, the compliance requirements are much simpler. For this reason, Cleo’s signup flow was way shorter than I expected. It only asked about my name, email, date of birth, and my US state. Then, all I needed to do was verify my email and connect my bank account whenever I wanted.

Besides that, there are more details I liked about this process:

- It first made it very clear what the app does before asking for my personal info (i.e., helping me track spending, save money, and build better habits).

- There are buttons inside the onboarding screens that clarify their data security conditions. It shows a tooltip explaining how my data is processed to help with my experience, as well as the fact that they don’t store login details.

- Their service is personalized. For example, they showed me a screen explaining that I can’t access cash advances and subscriptions due to my state’s laws.

Overall, it’s a good example of keeping onboarding simple through short inputs, clear value, and just enough reassurance. This is also the kind of experience we try to help teams build at Userpilot. Think of mobile onboarding patterns like slides and in-app flows that guide users without slowing them down.

Nevertheless, I’d only suggest such an approach for lower-risk fintech products like budgeting tools, expense trackers, or apps that don’t require full identity verification or direct fund transfers.

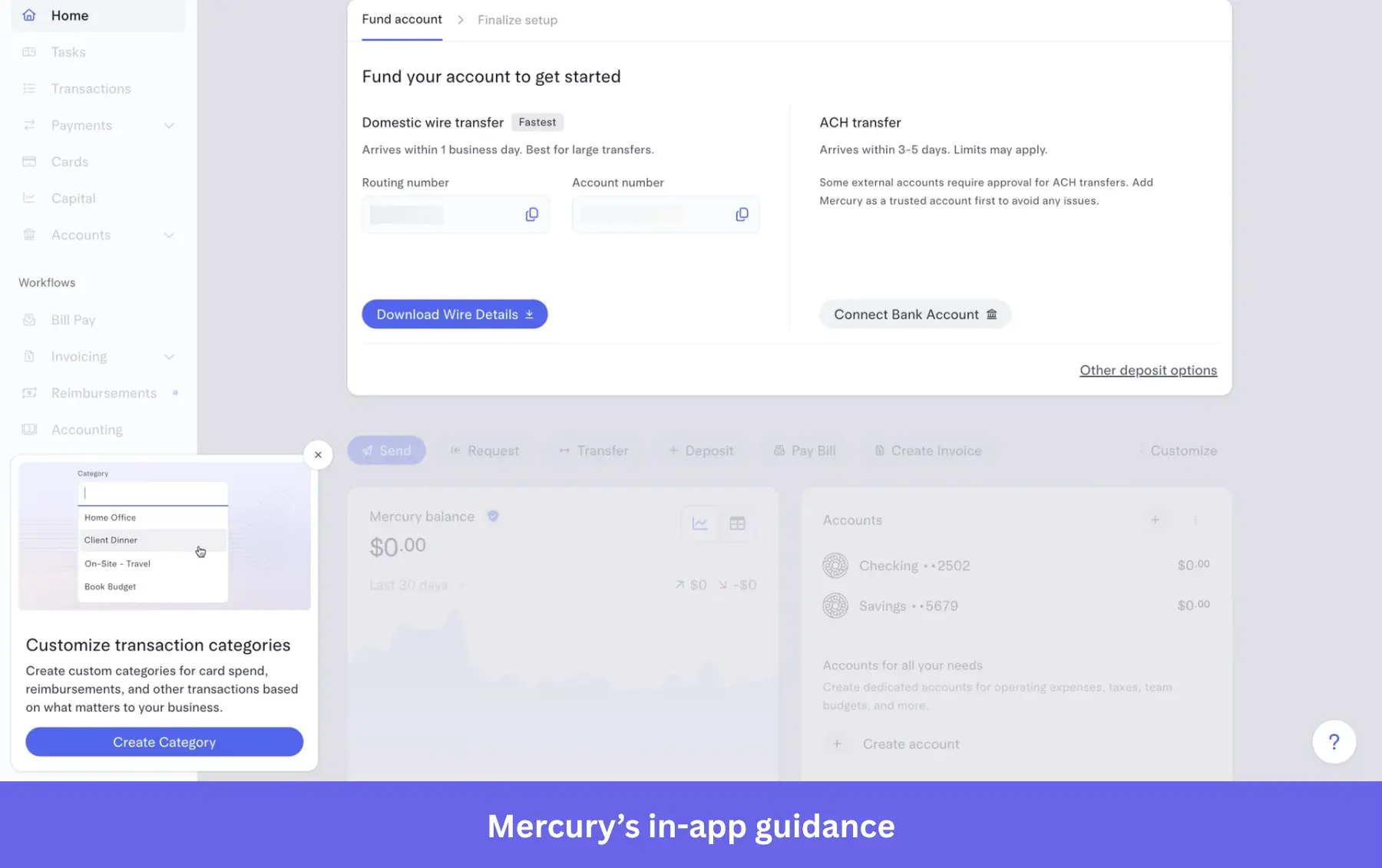

Mercury

Mercury is a banking app meant for startups and scaleups that lets you pay employees, open a bank account, get a card, etc.

I loved the fact that, unlike other banking apps, the signup flow was less tedious. It only asked for my business name, business type, and email.

Once I verified the email, it introduced me to a dedicated onboarding screen asking for more details, including extra company info, address, documentation, and ownership details. In my opinion, this is the best way to ask for additional information without making the first experience too overwhelming.

Another aspect I liked is that Mercury is one of the few platforms that includes in-app guidance. It showed a checklist for setting up my account with extra team members, linking cards, reimbursement management, and two-factor authentication. It also introduced features with tooltips as I was exploring the platform.

Pro tip: You can add similar in-app guidance inside web apps with user engagement tools like Userpilot.

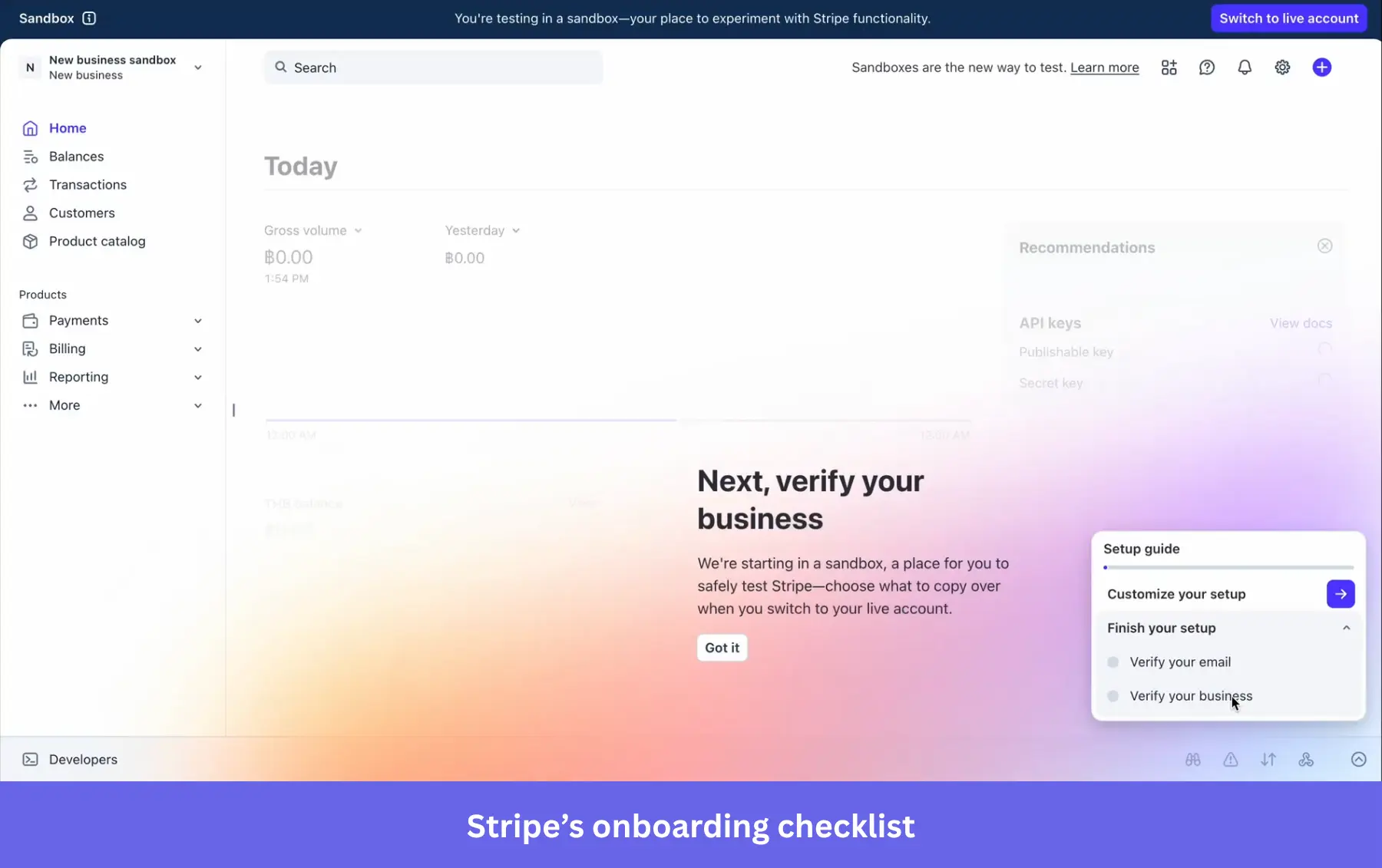

Stripe

My favorite aspect of Stripe’s onboarding is that it offers a unique sandbox-style onboarding flow. So instead of walking me through an endless signup process, it let me test the platform first and verify my information whenever I wanted.

It started by simply asking for my business name and website, which is skippable. Then, it sent me right inside the product, prompting me to follow its 2-step onboarding checklist.

Here, I could decide to ignore the checklist to experiment with Stripe features if I wanted. Once I felt like I could use the product for real transactions, I proceeded to complete the verification process.

However, despite this interesting onboarding style, I believe it missed adding interactive walkthroughs to introduce the core features first. It can feel a bit overwhelming to explore such a broad product without any direction.

What are the best practices for fintech onboarding?

Now, besides these examples, there are best practices to design fintech onboarding flows that aren’t too long, yet fulfill compliance requirements:

Progressive profiling

Drop-offs can spike dramatically once an onboarding screen contains four to five fields.

With “Progressive profiling” (don’t confuse with “progressive disclosure”), you only collect essential data at each stage and defer additional requirements until users engage deeper. This means that, rather than front-loading all verification, you only require an email to start, then request an SSN after the user attempts to open a brokerage account, and so on.

For instance, you can trigger a welcome survey asking new clients for their full name, then their ID when setting up their account, and finally proof of address before making a transaction.

Risk-based verification

This practice involves segmenting users based on geography, transaction volume, and funds to calculate their risk factor. And then, personalize the onboarding process based on risk, meaning low-risk users (with low income) get simplified eKYC, while high-risk profiles (corporate or high net-worth individuals) trigger full EDD.

Binance, for example, allows limited functionality with minimal verification, then escalates requirements as users access higher-value features.

Save-and-resume functionality

Since 38% of users abandon because they lack the required documents at the moment of application, allowing them to come back whenever they want is a must.

Going even further, you can also trigger re-engagement messaging within one hour of drop-off (e.g., progress-based reminders like “You’re 70% done”) to maximize activation rates.

Another easy example is to implement an onboarding checklist inside the app. This lets you break down the onboarding process into short steps that users can follow at their own pace.

AI-powered automation

AI is making its way into identity verification processes to make them shorter. This is because it can provide inline validation (i.e., telling users “Your ID image is too blurry” before submission) to prevent the delayed-rejection cycle that causes abandonment.

This automated KYC reduces compliance costs by 70% and cuts verification time by 80%. And as a result, some platforms might now complete onboarding in under 30 seconds with inline verification where the user never leaves the screen.

For example, the French fintech Shine achieves an 80% onboarding conversion rate through gamification elements, including progress bars, single-action screens, and digital confetti celebrating milestones.

Improve your fintech onboarding process with Userpilot!

I showed you examples of how popular fintechs onboard new customers. Yet, based on our experience with fintech clients, we know they could be better.

So if you’re interested in hiring an onboarding software to build a smoother first product experience, check our no-bs guide to choosing an onboarding tool in SaaS!

FAQ

What are the 4 pillars of fintech?

The four pillars of fintech refer to the core technology areas that power the financial technology industry, including Artificial Intelligence (AI), Blockchain, Cloud Computing, and Big Data.

This is because these technologies enable everything from automated lending decisions and fraud detection to real-time payment processing and personalized financial services.

What are the 5 stages of the onboarding process?

In the context of fintech and SaaS products, the five stages of the onboarding process are:

- The sign-up stage: Which focuses on getting users inside the product with minimal friction (where KYC and compliance steps already add extra barriers).

- The welcome and profiling stage: Where you collect key user data (like financial goals or company size) to personalize the experience.

- Product tour and education: The phase that introduces core features through interactive walkthroughs.

- Activation: Where users experience the product’s core value for the first time (reaching the “aha” moment).

- Habit forming (i.e., adoption): When users build your product into their daily workflow.

What are the 5 D's of fintech?

The 5 D’s of fintech describe the fundamental forces driving innovation in the industry, including:

- Digitization: Moving financial services from physical to digital channels (apps, cloud platforms, APIs).

- Disruption: Challenging traditional banking models with faster, cheaper, and more user-friendly alternatives.

- Democratization: Making financial services accessible to everyone regardless of income, location, or background.

- Decentralization. Using blockchain to distribute control away from central institutions.

- Data. Using big data and analytics to personalize services, manage risk, and optimize user experiences.

About the author